Item

Current Law

Trump Proposal

House Bill Passed May 22

Final Enacted Bill Passed by House and Senate

Individual income tax rates (Sec. 1)

Individual tax rates include: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. These rates expire after 2025 and revert to pre-TCJA rates.

The current rates would be made permanent; the individual income tax would be replaced by tariffs. The 39.6% rate would be reinstated on incomes over $1 million.

Extends the TCJA changes and provides an additional year of inflation adjustments for all brackets except the 35% and 37% brackets, effective after 2025.

Same as House but provides the additional year of inflation adjustments only to the 10% and 12% brackets.

Capital gains rate (Sec. 1(h))

Current capital gains rates:

Short-term capital gains are taxed at ordinary rates;

Long-term capital gains rates (without net investment income tax):

- 0% for taxpayers with income up to $94,050 (MFJ), $47,025 (S), and $63,000 (HOH)

- 15% for taxpayers with income between $94,051 to $583,750 (MFJ), $47,026 and $518,900 (S), and $63,001 and $551,350 (HOH)

- 20% for taxpayers with income over $583,750 (MFJ), $518,900 (S), and $551,350 (HOH)

Collectibles: 28%

Rate thresholds are scheduled to change in 2026.

The top LTCG rate would be reduced to 15% and bracket thresholds made permanent. Cryptocurrency would be exempt from capital gains tax.

No change except making the current bracket thresholds permanent.

Same as House.

Standard deduction (Sec. 63)

For 2025:

- $31,500 (MFJ),

- $15,000 (S/MFS),

- $22,500 (HOH).

Increased amounts expire after 2025.

The Trump proposal would increase these amounts and make the increases permanent.

Makes permanent the increased standard deduction under TCJA, with an additional year of inflation adjustment, and temporarily increases the deduction for four years from 2025 through 2029 by $2,000 (MFJ), $1,500 (HOH), and $1,000 (S/MFS).

Permanently increases the standard deduction beginning in 2025 to $32,000 (MFJ), $15,750 (S), and $23,625 (HOH).

Personal exemptions (Sec. 151)

Personal exemptions are at zero through 2025.

Personal exemptions would remain at zero permanently.

Permanently repeals personal exemptions.

Same as House, except a new personal exemption is created for seniors to replace the House deduction, discussed below.

Child tax credit (Sec. 24)

Maximum child tax credit (CTC) is $2,000 per qualifying child; up to $1,700 per child can be refundable. CTC is reduced by $50 for each $1,000 of income above the following levels:

- $200,000 of modified adjusted gross income (MAGI) for single filers

- $400,000 MAGI for joint filers. CTC reverts to $1,000 per qualifying child after 2025, with a higher refund earned income threshold and lower phaseout levels.

Vice President JD Vance suggested increasing the CTC to $5,000 per child regardless of income level.

Increases the CTC to $2,500 per child from 2025 through 2028. The CTC would revert to $2,000 in 2028, adjusted for inflation. The refundable portion of the CTC would be made permanent.

Permanently increases the CTC to $2,200 beginning in 2025, indexing it to inflation thereafter. Makes permanent the refundable portion of the CTC.

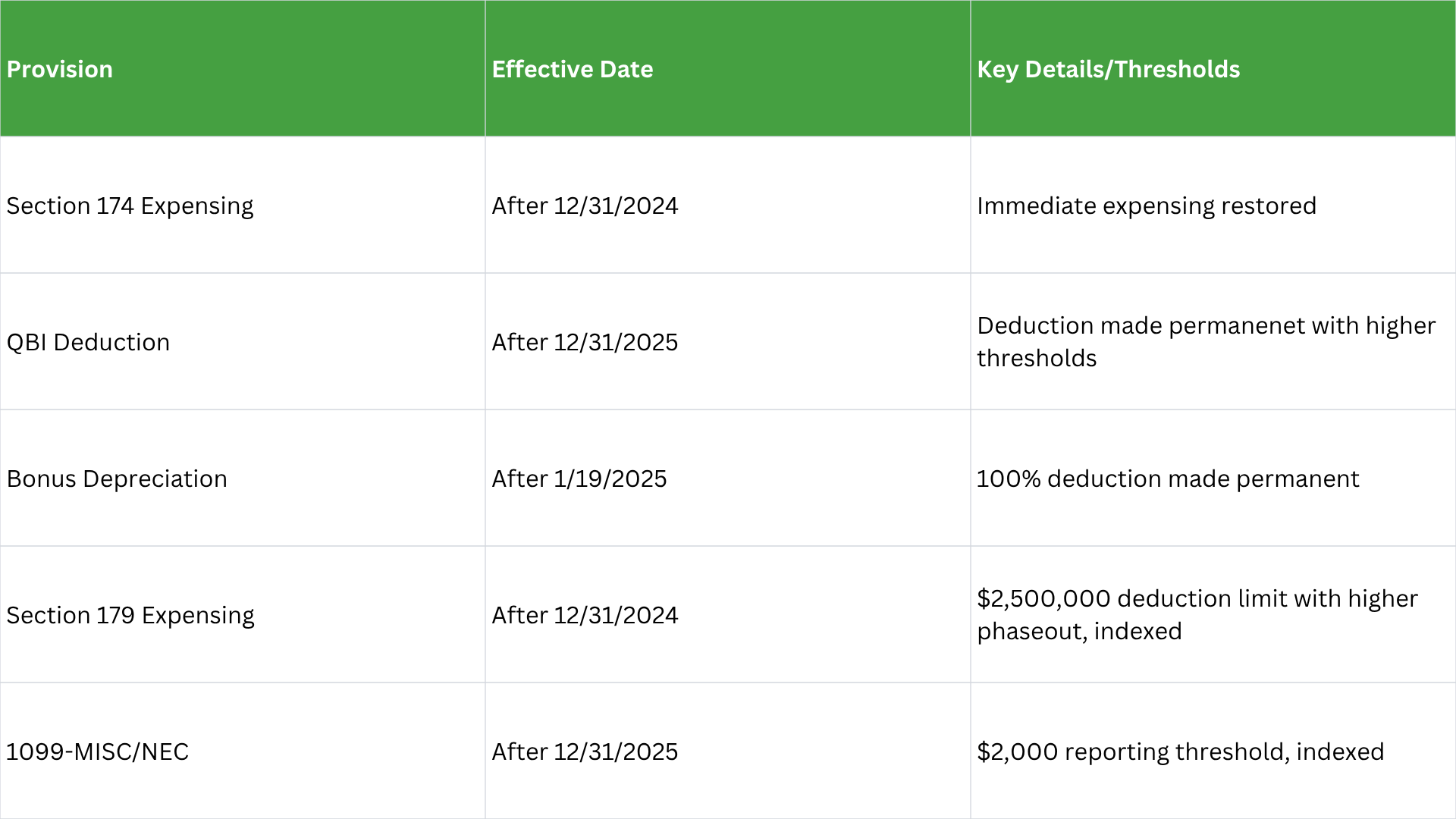

Qualified business income deduction (Sec. 199A)

Individuals, fiduciaries, and trust/estate beneficiaries may deduct 20% of qualified business income from a partnership, S corporation, or sole proprietorship (20% of total qualified real estate investment trust dividends and publicly traded partnership income are also eligible). There is no cap on the deduction; however, the deduction is subject to income limitations. In 2024, the deduction phases out for incomes between $191,950 and $241,950 (single filers) and between $383,900 and $483,900 (joint returns) in 2024. Provision expires after 2025.

The current rule would be made permanent.

Makes the deduction permanent at an increased 23% rate with a change to the phaseout rules for nonqualified income. Extends deduction to business development companies, and other modifications effective after 2025.

Makes deduction permanent at 20% rate with slightly different change to the phaseout rules for nonqualified income than the House.

Creates new minimum $400 deduction for taxpayers with at least $1,000 of qualified income, with both figures indexed to inflation.

Alternative minimum tax (AMT) exemptions and phaseouts (Sec. 55)

The TCJA increased exemption from 2018 through 2025. Exemptions in 2025:

- $137,000 (MFJ)

- $88,1000 (S/HOH)

- $68,500 (MFS)

Phaseout of AMT:

- $1,252,700 (MFJ)

- $68,500 (MFS)

The increased exemption amounts would be made permanent.

Generally makes the TCJA AMT thresholds permanent, but only after resetting the inflation adjustments back to the 2018 level, effectively reducing the thresholds and reindexing them to inflation after 2026. The amounts in 2026 would be reduced to:

- $109,400 (MFJ)

- $70,300 (S/HOH)

- $54,700 (MFS)

Phaseout of AMT:

- $1,000,000 (MFJ)

- $500,000 (S/HOH/MFS)

Same as House but only the phaseout thresholds would be reset to the 2018 level, not the exemption amounts, and the phaseout of the exemptions based on the amount of income exceeding the thresholds would be slowed by half.

Deduction for qualified residence interest (Sec. 163(h))

For indebtedness incurred after December 31, 2017, and before January 1, 2026, taxpayers may treat no more than $750,000 ($375,000 if MFS) as acquisition indebtedness for purposes of the mortgage interest itemized deduction. For indebtedness incurred on or before December 31, 2017, and for all acquisition indebtedness on or after January 1, 2026, the indebtedness amounts are $1 million ($500,000 if married filing separately).

The lower indebtedness amounts would be made permanent.

Makes permanent the lower cap on indebtedness.

Same as House but treats certain mortgage insurance premiums as qualified interest.

Casualty loss deduction (Sec. 165(c))

Personal casualty losses incurred after December 31, 2017, and before January 1, 2026, are generally not deductible under the TCJA (except to the extent of personal casualty gains) unless they are disaster losses, which remain deductible under the TCJA to the extent the loss exceeds 10% of AGI.

The casualty loss limitations would be made permanent.

Makes the casualty loss limitations under the TCJA permanent.

Same as House but extends the exception for disaster loss treatment to state-declared disasters.

Other itemized deductions (Sec. 63)

From 2018 through 2025:

- Medical/dental expenses if they exceed 7.5% of AGI

- Charitable contributions generally up to 60% of AGI

- Misc. itemized deductions suspended

Itemized deduction limitations would be made permanent.

Makes limits on itemized deduction limits permanent.

Similar to House but allows an itemized deduction for certain educator expenses.

Pease limitation on itemized deduction

The Pease limit on itemized deductions is suspended under the TCJA for 2018 to 2025.

The repeal of the limitation would be made permanent.

Makes the repeal of the Pease limitation permanent but would create a new limitation in its place. The new limit would generally cap the value of itemized deductions so that the maximum benefit would be equivalent to reducing taxable income in the 32% bracket rather than in the 35% and 37% brackets.

Same as House but the new limit would only cap the value at the 35% bracket rather than the 32% bracket.

Charitable deduction (Sec. 170)

The individual deduction for charitable contributions is available only for taxpayers that itemize their deductions. For 2021, a temporary provision allows a charitable deduction of up to $300 for non-itemizing taxpayers.

No specific proposal.

Reinstates a deduction for charitable contributions for taxpayers that do not itemize of up to $300 (MFJ) or $150 (S, HOH, MFS) for years 2025-2028.

Reinstates a permanent charitable deduction for nonitemizers beginning in 2026 of up to $1,000 (S, HOH, MFS) or $2,000 (MFJ). Creates a new 0.5% floor on itemized charitable deductions that limits the deduction to the amount exceeding 0.5% of the deductible base.

Other TCJA limits

From 2018 through 2025:

- Limit on deducting wagering losses

- Limit on exclusion and deduction of wagering losses

- Repeal of exclusion for bicycle commuting reimbursements

- ABLE account changes

- Exclusion for student loan forgiveness after death

- Treatment of service on Sinai Peninsula

Make TCJA limits permanent.

All listed TCJA changes would be made permanent.

Same as House, but would restore the ability to deduct up to 90% of wagering losses (up to wagering income).

Taxation of carried interest (Sec. 1061)

Treated as long-term capital gain (top rate 20%) if held over three years (TCJA); otherwise taxed at ordinary rates.

Tax carried interest as ordinary income.

No provision.

No provision.

Taxation of Social Security benefits (Sec. 86)

- 0% is taxed if combined income (AGI + nontaxable interest + half SS benefits) is below $32,000 (MFJ) or $25,000 (S)

- Up to 50% is taxed if combined income is between $32,000 and $44,000 (MFJ) or $25,000 and $34,000 (S)

- Up to 85% is taxed if combined income exceeds $44,000 (MFJ) or $34,000 (S)

All Social Security benefits would be exempt from tax.

Creates a $4,000 income tax deduction for taxpayers aged 65 and above for four years from 2025 through 2028. Deduction would be available without regard to whether deductions are itemized, but phases out beginning with MAGI exceeding $150,000 (MFJ) and $75,000 (S/HOH/MFS).

Creates a $6,000 personal exemption for taxpayers aged 65 and above for four years from 2025 through 2028. Exemption would phase out with MAGI exceeding $150,000 (MFJ) and $75,000 (S/HOH/MFS).

Taxation of tip income (Sec. 61)

Tip income is taxed under Sec. 61 and reported to employers monthly under Sec. 6053.

Tips would be exempt from income tax and potentially employment tax.

Creates an income tax deduction equal to reported tip income from 2025 through 2028. Deduction would be available only for voluntary tips in occupations that “traditionally and customarily” received tips before 2025 in a business that is not a specified service trade or business under Section 199A. Deduction would be available without regard to whether deductions are itemized but only to taxpayers with income below the threshold for “highly compensated employees” under Section 414 ($160,000 in 2025). The provision would also extend the FICA tip credit to cover certain beauty services.

Same as House provision but deduction would be capped at $25,000 and would phase out for MAGI exceeding $150,000 (S) or $300,000 (MFJ).

Taxation of overtime pay (Sec. 61)

Overtime pay is subject to income and employment tax.

Overtime pay would be exempt from income and employment taxes.

Creates an income tax deduction equal to overtime pay under the FLMA from 2025 through 2028. Deduction would be available without regard to whether deductions are itemized but only to taxpayers that are not “highly compensated employees” under Section 414 ($160,000 in 2025).

Same as House provision but deduction would be capped at $12,500 (S) or $25,000 (MFJ), and phase out for MAGI exceeding $150,000 (single) or $300,000 (joint).

Auto loan interest deduction

There is no current deduction for personal interest, which includes interest incurred on a personal vehicle loan.

Interest on loans for domestic vehicles would be deductible.

Creates an above-the-line deduction for up to $10,000 in interest paid on a loan for vehicles with final assembly in the U.S. Deduction would phase out when modified AGI exceeds $100,000 (S) or $200,000 (MFJ). Effective for tax years 2025 through 2028.

Same as House except the deduction would be available for nonitemizers instead of as an above-the-line deduction.

State and local tax (SALT) cap (Sec. 164)

SALT itemized deductions limited to $10,000 ($5,000 MFS) of state and local income, property, and sales taxes through 2025.

The SALT deduction cap would be eliminated.

Makes SALT cap permanent at an increased threshold of $40,000, beginning in 2025. The 40,000 threshold would phase down to $10,000 for income exceeding $500,000. These thresholds would increase by 1% each year from 2026 to 2033. The provision would also largely shut down state PTET workaround regimes unless 75% of the entities’ gross receipts come from a qualifying trade or business under Section 199A.

Sets a $40,000 SALT cap for 2025 that would phase down to $10,000 for income exceeding $500,000. These thresholds would increase by 1% each year from 2026 through 2029. In 2030, the SALT cap would revert to $10,000.

Credit for caregivers

No provision.

A tax credit for caregivers would be provided.

No provision.

No provision.

Eliminate double taxation of Americans abroad

Individuals may exclude foreign earned income from U.S. tax up to a threshold indexed to inflation ($130,000 in 2025).

Provide increased or unlimited exemption from U.S. tax on foreign income.

No provision.

No provision.

Active loss limit (Sec. 461)

Section 461 limits a taxpayer’s ability to deduct certain active business losses above a limit that is indexed to inflation and in 2025 reached $626,000 (MFJ) and $313,000 (S/HOH/MFS). The limited loss generally becomes an NOL in future years. The provision is set to expire for tax years beginning after Dec. 31, 2028.

No specific provision.

Makes the active loss limit under Section 461(l) permanent, while requiring losses arising from the limit to be tracked separately and applied as part of the Section 461(l) calculation in future years.

Makes the active loss limit under Section 461(l) permanent while reducing the threshold at which the limit applies.

Tax-preferred savings accounts

The tax code provides for some tax-preferred savings and spending accounts.

No specific provision.

Creates a new type of tax-preferred account for minors. Contributions would be capped annually at $5,000 and would not be deductible, but the accounts would generally be exempt from tax, with qualified distributions taxed as capital gains. Under a pilot program, children born from 2025 through 2028 would receive a $1,000 contributory credit in their account.

Same general provision as House, with some minor and technical modifications.

Lifetime exemption amount (Secs. 2010, 2505)

Lifetime exemption amount set at $10 million indexed to inflation ($13.99 million in 2025). The top estate tax rate is 40%. Exemption amount would be cut in half in 2026. 40% rate is permanent.

The exemption amount would be increased and made permanent (or the estate tax would be repealed in full).

Exemption amount would be increased to $15 million per taxpayer in 2026 and indexed for inflation thereafter.

Same as House.

.jpg)

.png)

.png)

.png)

.jpg)

.jpg)